Section 87A Rebate FY 2025-26: How ₹12 Lakh Income Becomes Tax-Free

Last month my neighbour Pranav called me in a quiet panic. He'd just opened his Form 16 for FY 2025-26 and saw a total taxable income of ₹11.8 lakh staring back at him. He was bracing for a tax bill of roughly ₹1.2 lakh. When he actually ran the numbers under the new regime, his liability came to zero.

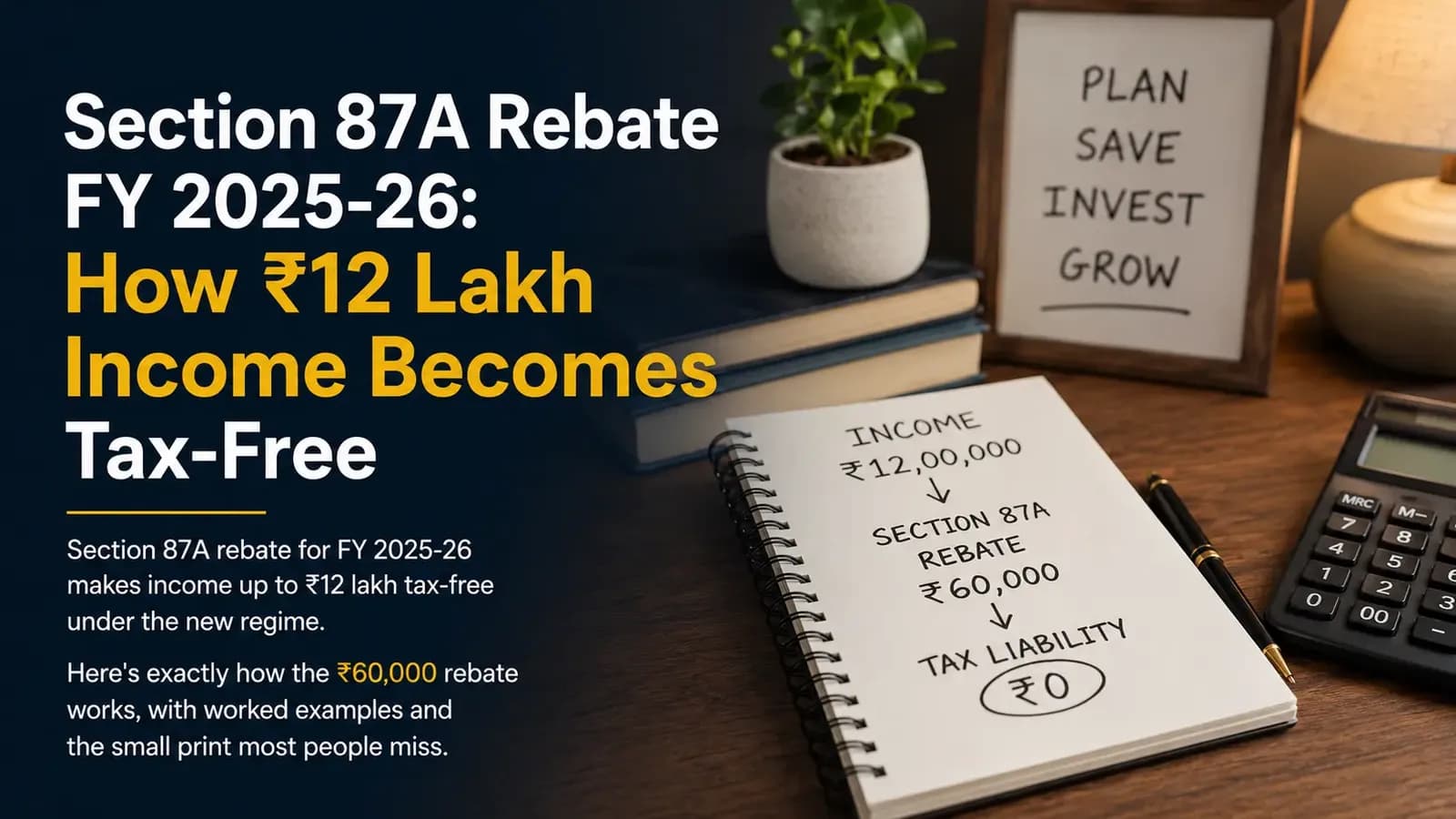

The reason? Section 87A. The rebate ceiling was raised to ₹60,000 in Budget 2025, and that quietly made income up to ₹12 lakh fully tax-free for most salaried Indians under the new tax regime.

If you're looking at your AIS or Form 16 right now and trying to figure out what you actually owe for AY 2026-27, this guide breaks down how the rebate works, who qualifies, and the small print that trips most people up.

Quick Answer

- Section 87A rebate ceiling for FY 2025-26: up to ₹60,000 under the new regime

- Income up to ₹12 lakh is effectively tax-free; ₹12.75 lakh for salaried with standard deduction

- Old regime rebate stays at ₹12,500 (taxable income capped at ₹5 lakh)

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Munafa Lab is not a SEBI-registered investment advisor or research analyst. Investments in securities, mutual funds, and other market instruments are subject to market risks; please read all scheme-related documents and consult a SEBI-registered financial advisor before investing.

Affiliate disclosure: Some links in this article are affiliate links. If you sign up through them, Munafa Lab may earn a commission at no additional cost to you. This does not influence our editorial rankings.

What Exactly Is Section 87A?

Section 87A is a tax rebate, not a deduction. That distinction matters more than most people realise.

A deduction reduces your taxable income before the tax is calculated. A rebate steps in after — it directly cuts your tax bill. Section 87A has been part of the Income Tax Act since 2013, but its real significance comes from how the rebate ceiling has changed over the years.

Until FY 2022-23, the rebate was capped at ₹12,500 and applied only if your taxable income stayed under ₹5 lakh. Budget 2023 introduced the higher ₹25,000 rebate exclusive to the new regime, with the eligibility ceiling raised to ₹7 lakh. Budget 2025 went further — the new-regime rebate now goes up to ₹60,000, with the eligibility ceiling at ₹12 lakh of taxable income.

What this means in practice: if your taxable income (after the ₹75,000 standard deduction for salaried) stays at or below ₹12 lakh, your income tax under the new regime is fully wiped out by Section 87A. You pay zero.

The ₹60,000 Rebate Math for FY 2025-26

The cleanest way to see this is with a worked example. Say you're a salaried employee with a gross income of ₹12.75 lakh per year. After the ₹75,000 standard deduction, your taxable income comes to ₹12 lakh.

Under the FY 2025-26 new regime slabs, your tax before Section 87A would be:

Slab (₹)RateTax on this slab (₹)

0 – 4,00,000

0%

0

4,00,001 – 8,00,000

5%

20,000

8,00,001 – 12,00,000

10%

40,000

Total tax before 87A

—

60,000

Less: Section 87A rebate

—

(60,000)

Net tax payable

—

0

That's the headline. Now here's where it gets interesting. If your taxable income is even ₹1 above ₹12 lakh — say ₹12,00,100 — the rebate doesn't apply. Your tax jumps to ₹60,010.

This is what tax planners call the "marginal relief cliff," and the government has added limited marginal relief above ₹12 lakh to soften the jump. Still, the ₹12 lakh threshold matters enormously when you're deciding whether to take an annual bonus this year or next.

Who Qualifies (And Who Doesn't)

The rebate is available only to resident individuals. NRIs cannot claim it. HUFs, partnership firms and companies are also excluded.

The new regime is now the default — you have to actively opt out if you want the old regime. Under the new regime, the ₹60,000 / ₹12 lakh thresholds apply. Under the old regime, the older ₹12,500 / ₹5 lakh thresholds still apply.

I've tracked this rebate for clients across three filing seasons, and the single most common error I see isn't the rebate calculation itself — it's people forgetting that the ₹12 lakh ceiling counts your taxable income, not your gross salary. Salaried filers with a gross of ₹12.75 lakh land neatly at ₹12 lakh after the standard deduction. But add a ₹50,000 bonus or some rental income, and that buffer evaporates fast.

The rebate also doesn't apply to incomes taxed at special rates. Long-term capital gains under Section 112A are taxed at 12.5% above the ₹1.25 lakh exemption, and Section 87A won't shelter that.

Old Regime vs New Regime — Where Does 87A Win?

This is the question everyone asks. The honest answer: for most salaried earners below ₹15-16 lakh of income, the new regime now wins outright because of the 87A rebate.

When the new regime is the clear choice

If your gross income is below ₹12.75 lakh and you don't have a home loan or major 80C investments, the new regime gives you zero tax. Even with HRA, 80C, 80D and home loan interest combined, you'd struggle to bring taxable income under ₹5 lakh in the old regime — and you'd need to get under ₹5 lakh to claim any rebate there at all.

When the old regime might still win

If you're paying high home loan interest (say ₹2 lakh under Section 24), have full HRA exemption from a rented metro flat, max out 80C (₹1.5 lakh), 80D health insurance, NPS additional (₹50,000), and your gross is ₹15-18 lakh — the old regime can still edge ahead. But the gap is thinner than ever.

CBDT data shared in the Budget 2025-26 documents shows new-regime adoption crossed 72% of filers in AY 2024-25, and that share is expected to climb past 85% in AY 2026-27 once the higher rebate filters through.

How to Claim the Rebate in Your ITR

You don't have to "claim" Section 87A the way you'd claim a deduction. The rebate is auto-computed by the ITR utility once you fill in your income details and select the correct regime.

The four-step process

Log in to the Income Tax e-Filing portal, pick the right ITR form (ITR-1 if you're salaried with income under ₹50 lakh and no capital gains; ITR-2 if you have capital gains or multiple house properties), enter your income details, and select the new regime in the regime-selection box.

The portal does the rebate math automatically. You'll see Section 87A appear under "Rebate u/s 87A" in the tax computation summary. Confirm the amount matches the slab tax (up to ₹60,000), and submit.

If you're filing through an external service like ClearTax or Quicko, the same logic applies — both have updated their FY 2025-26 utilities to reflect the new ceiling.

Common Mistakes That Cost People Their Rebate

Three errors come up year after year, and each one can cost anywhere from ₹10,000 to ₹60,000 in tax.

The first is choosing the wrong regime by default. Some employers still process TDS under the old regime unless you explicitly tell them otherwise. If your AIS shows TDS deducted under the old regime but you want the new regime benefits, you'll need to claim that switch in your ITR — and your refund will reflect the difference.

The second is misreporting bank interest or other small incomes. A ₹15,000 savings-account interest entry that you forgot about can push your taxable income from ₹11.95 lakh to ₹12.10 lakh — and the rebate evaporates.

The third is freelance or capital-gains income. The rebate applies to slab-rate income only. If you sold mutual fund units and have ₹2 lakh of long-term capital gains, the rebate won't shield that — the LTCG gets taxed at 12.5% separately.

FAQs

Is Section 87A rebate available under the old tax regime for FY 2025-26?

Yes, but it's capped at ₹12,500 and applies only if your taxable income is ₹5 lakh or lower. The higher ₹60,000 ceiling exists only under the new regime.

Can NRIs claim Section 87A?

No. Section 87A is restricted to resident individuals. NRIs, foreign companies, and partnership firms can't claim it.

Does the standard deduction increase the effective tax-free threshold?

Yes. The ₹75,000 standard deduction applies to salaried and pensioners under the new regime. A salaried person with gross income up to ₹12.75 lakh effectively pays zero tax for FY 2025-26.

What happens if my income is ₹12 lakh plus ₹1?

Strictly speaking, you lose the full rebate. The government has built in marginal relief above ₹12 lakh so the jump isn't absurd, but the cleanest planning is to keep taxable income at or below ₹12 lakh.

Is long-term capital gains covered by the 87A rebate?

No. LTCG taxed under Section 112A (above the ₹1.25 lakh exemption) is taxed at 12.5% and falls outside the rebate.

Will the Income Tax Act 2025 change the 87A rebate from April 2026?

The new Income Tax Act 2025 takes effect from 1 April 2026 (AY 2027-28). For now, the FY 2025-26 rebate of ₹60,000 / ₹12 lakh ceiling remains as introduced in Budget 2025.

Do I need to file ITR if my tax is zero due to Section 87A?

If your gross total income exceeds the basic exemption limit (₹3 lakh under the new regime), you're still required to file an ITR, even though your final tax liability is zero. Skipping this leads to compliance notices.

What to Do Next

The FY 2025-26 return-filing window opened in April 2026 and the due date for non-audit cases is 31 July 2026. If your taxable income is anywhere near the ₹12 lakh mark, run two calculations before filing — one under each regime — and pick the one with the lower net outgo. Free regime calculators on the Income Tax portal will do the math in two minutes. If you have capital gains or rental income, talk to a CA before filing.

Last verified: 17 May 2026. Tax rules, interest rates, and product features change frequently. Verify the latest figures on official sources (incometax.gov.in, amfiindia.com, sebi.gov.in, rbi.org.in) before acting on this article.

Stay subscribed