Credit Card ₹10 Lakh Rule 2026: When Your Spending Goes to Income Tax

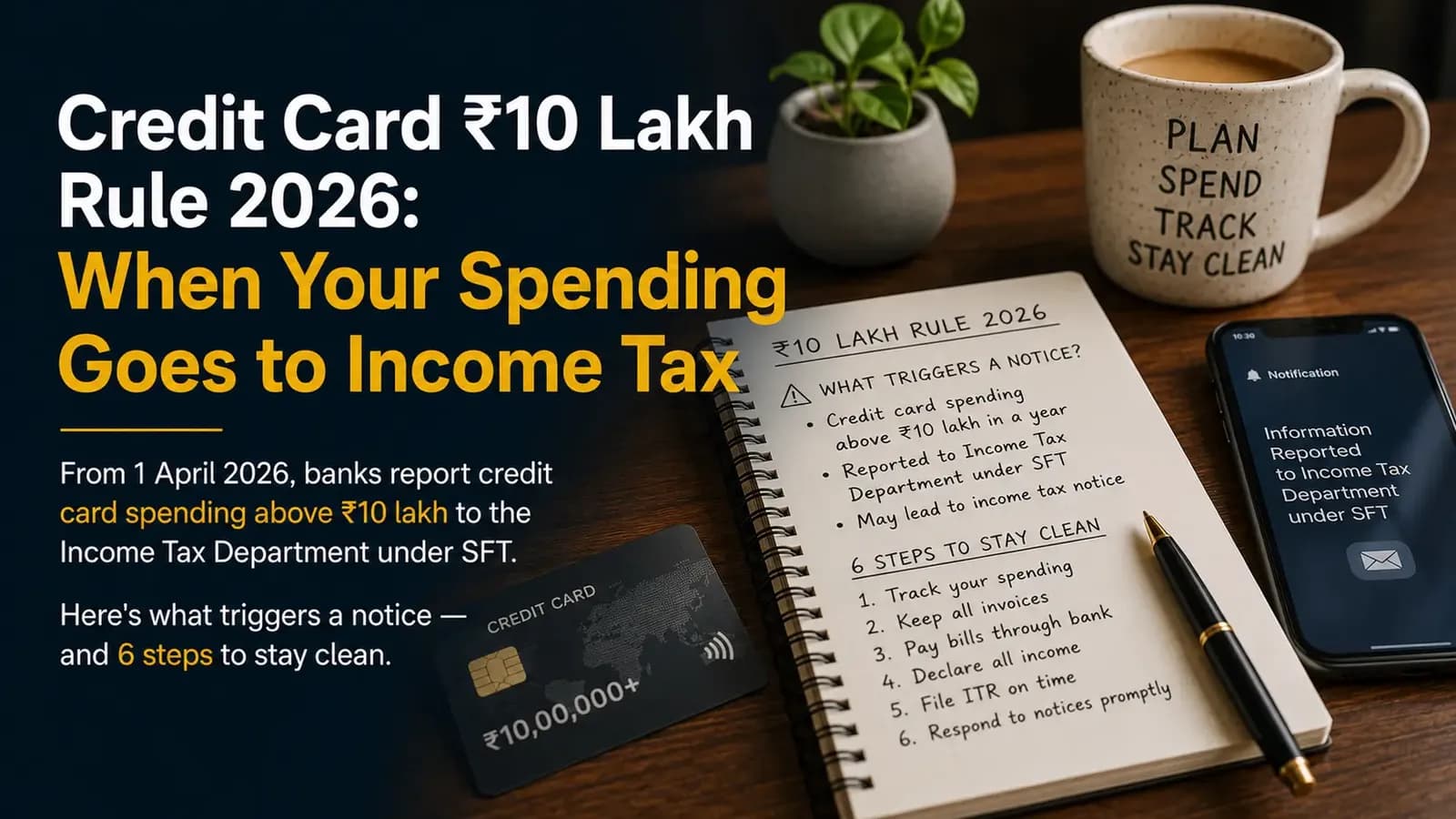

From 1 April 2026, the new Income Tax Act 2025 took effect — and with it, the most consistent enforcement of the credit card ₹10 lakh rule India has seen.

If your total credit card bill payments cross ₹10 lakh in a financial year, your bank reports it to the Income Tax Department under the Statement of Financial Transactions (SFT) framework.

This isn't a new rule. It already existed for years.

What changed is the enforcement layer:

- Faster AIS updates

- Automated reporting

- Stronger income-vs-spending cross-checks

For most people, daily life changes absolutely nothing.

But if you spend heavily on:

- Travel

- Weddings

- Business expenses through personal cards

…then this is the year to keep your paperwork clean.

Quick answer: If your annual credit card bill payments cross ₹10 lakh with a bank, the bank reports it to the Income Tax Department under SFT rules. This is not a new tax. But if your declared income doesn't justify the spending, you may receive a Section 133(6) notice asking for clarification.

Disclaimer: This article is for educational purposes only and does not constitute investment advice.

What Changed on 1 April 2026

The Income Tax Act 2025 replaced the older 1961 tax framework for FY 2026-27 onwards.

Three important credit card reporting rules became more tightly enforced:

- ₹10 lakh SFT reporting threshold confirmed for non-cash credit card payments

- Cash payments above ₹1 lakh on credit card bills remain reportable

- PAN linkage mandatory for card issuance and renewals

Banks must now file these reports automatically through Form 61A before 31 May every year.

The AIS system also updates faster than before.

That means your spending becomes visible to the tax department much earlier than in previous years.

How the ₹10 Lakh Credit Card Rule Actually Works

Most people misunderstand the trigger.

The rule is based on:

Annual Credit Card Bill Payments

Not monthly spending.

Not reward points.

Not EMI limits.

Important Clarifications

1. Threshold Applies Per Bank

If you have:

- 2 HDFC cards

- 1 HDFC add-on card

…and combined bill payments cross ₹10 lakh, HDFC reports the total figure.

2. Payments Matter, Not Statements

The system tracks:

- Bill payments

- Advance payments

- Prepayments

- Settlements

Even pre-bill payments count.

3. AIS Combines Everything

Each bank reports separately.

But your AIS dashboard shows the complete combined picture.

The Income Tax Department sees all reported spending together.

Reporting Does NOT Mean Automatic Tax Notice

This is the biggest myth.

Crossing ₹10 lakh does NOT automatically generate a tax notice.

The SFT entry simply appears inside AIS.

A notice usually happens only if:

- Income looks too low compared to spending

- Transactions appear suspicious

- Large unexplained gaps exist

Common notice sections:

- Section 133(6)

- Section 143 queries

Myth vs Reality — Credit Card ₹10 Lakh Rule

MythActual RealityWhat You Should Do

₹10 lakh spend means automatic notice

It's only a reporting trigger

Check AIS regularly

All cards combine automatically

Threshold applies bank-wise

Track spending bank-by-bank

Forex spending isn't tracked

International spending is also visible

Track overseas usage

Add-on cards are separate

Linked to primary PAN holder

Avoid routing family expenses

Company cards don't matter

Personal usage may become taxable

Keep business proof ready

Real Spending Patterns That Trigger Scrutiny

The threshold itself is mechanical.

The context behind the spending matters more.

1. Business Spending on Personal Cards

Example:

- Salary income: ₹14 lakh

- Credit card payments: ₹22 lakh

The department may assume undeclared business income.

Best practice:

- Separate business cards

- Separate business accounts

2. Heavy International Travel Without Documentation

Example:

- ₹4 lakh international travel

- Claimed as office reimbursement

- No supporting proof

This can become taxable salary/perquisite income.

3. Early-Career High Spending

Example:

- Salary: ₹8 lakh

- Annual card payments: ₹14 lakh

Even if family funded it, documentation becomes important.

Maintain:

- Gift records

- Transfer proofs

- Family declarations

4. Jewellery or Gold Purchases

Large jewellery transactions can trigger:

- Card SFT reporting

- Separate jewellery transaction monitoring

Especially above ₹2 lakh.

5. International ATM Cash Withdrawals

Frequent overseas cash advances remain highly monitored categories.

Other Credit Card Changes in 2026

The ₹10 lakh reporting rule isn't the only update.

Several banks changed reward structures too.

SBI Cashback Card

- Cashback cap reduced from ₹5,000 to ₹4,000 monthly

- Online and offline caps split separately

SBI Rent Payments

Reward points on rent payments discontinued from April 2026.

HDFC Regalia Gold

- Reward rate revised

- Lounge access now requires quarterly spending targets

HDFC Infinia Metal

Annual retention requirement increased significantly.

Weekly CIBIL Reporting

Banks now update credit bureau data every 7 days instead of monthly.

Missed payments affect credit scores faster.

Mandatory Two-Factor Authentication

Now required on:

- Online transactions

- POS machine payments

As per RBI directions.

6-Step Playbook for Heavy Credit Card Users

If you spend above ₹10 lakh yearly, do these quarterly.

Step 1 — Check AIS

Login to the income tax portal.

Open:

AIS → Statement of Financial Transactions

Review exactly what banks reported.

Step 2 — Compare Spend vs Income

Simple rule:

Your annual card spend should broadly match your post-tax income level.

If not, maintain proof explaining the difference.

Examples:

- Savings usage

- Family gifts

- Loans

Step 3 — Separate Business and Personal Spending

Never mix:

- Client expenses

- Office purchases

- Family spending

on one personal card.

Step 4 — Maintain Gift Documentation

Large family transfers should always have:

- Bank records

- Gift letters

- Supporting transaction proof

Step 5 — File ITR Properly

File:

- ITR-1

- ITR-2

- ITR-3

based on actual eligibility.

AIS mismatches reduce significantly when returns are filed correctly.

Step 6 — Preserve Statements for 7 Years

Tax reassessment windows can stretch multiple years backward.

Save:

- Annual statements

- Payment proofs

- Bank records

offline too.

FAQs

What is the credit card ₹10 lakh rule?

Banks report annual credit card bill payments above ₹10 lakh under SFT rules to the Income Tax Department.

Is it a new tax?

No.

It is only a reporting requirement.

Will I automatically get a notice?

No.

Notices usually happen only when spending and declared income don't match.

Is the limit per card or per bank?

Per bank.

Multiple cards from the same bank are combined.

Are international payments included?

Yes.

Foreign transactions are also tracked.

Do advance bill payments count?

Yes.

Prepayments and advance settlements are included.

What if I use a company card personally?

Personal usage on company cards may become taxable salary/perquisite income.

How do I check reported credit card data?

Login to the Income Tax portal and open AIS → SFT Information.

Final Thoughts

The ₹10 lakh rule is not designed to punish spenders.

It's mainly a transparency system.

If your:

- Income

- AIS

- Credit card spending

- ITR filing

all tell the same story, then the SFT entry becomes just another data point.

Pull your AIS once every quarter, compare it with your statements, and fix mismatches early instead of waiting for notice season.

Stay subscribed